1.1 Introduction to Business

- All human beings require various goods and services to satisfy their needs, which are typically acquired from markets (physical or electronic).

- The provision of these goods and services is carried out through economic activities such as production, manufacturing, distribution, and exchange, aiming to satisfy customer needs and wants.

- Business is a primary economic activity focused on the production and sale of goods and services demanded by people. It is central to daily life and involves a process from production to consumption.

- The entire scope of business encompasses industry, trade, and commerce.

1.1.1 Role of Business in the Development of Economy

- Business, including trade and commerce, has historically been crucial to economic prosperity, as evidenced by ancient trading activities in India via land and water routes (e.g., Silk Route).

- Ancient Indian trade generated surplus income, fostering various economic activities and leading to the growth of indigenous banking systems, exemplified by the use of “Hundi” and “Chitties” for safe money transfer.

- Credit transactions, loans, and advances further boosted commercial operations.

- India historically maintained a favorable balance of trade, with exports exceeding imports, which supported manufacturers, traders, and merchants.

- Significant ancient trade centers included Pataliputra, Peshawar, Taxila, Indraprastha, Mathura, Varanasi, Mithila, Ujjain, Surat, Kanchi, Madura, Broach, Kaveripatta, and Tamralipti.

- The Indian subcontinent was referred to as ‘Swaran Bhoomi and Swaran Deep’ by various travelers due to its prosperity from trade.

- The British Empire’s advent shifted India from an exporter of processed goods to an exporter of raw materials and importer of manufactured goods.

- Post-independence, India aimed for self-reliant socialistic development, focusing on public investment in industries and technological advancements.

- Economic liberalization in 1991 addressed challenges like weak financial systems and high fiscal deficits, leading to a three-pronged approach of stabilization, restructuring, and globalization.

- Today, India is a fast-growing economy and a preferred FDI destination, with government initiatives like ‘Make in India,’ ‘Skill India,’ and ‘Digital India’ contributing to its growth.

1.2 Concept of Business

- The term “business” is derived from “busy” and broadly refers to an occupation involving regular engagement in purchase, production, and/or sale of goods and services for profit.

- Human activities are categorized into:

- Economic Activities: Undertaken to earn a livelihood (e.g., a factory worker, doctor, teacher). These are further divided into business, profession, and employment.

- Non-Economic Activities: Performed out of love, sympathy, sentiment, or patriotism (e.g., a housewife cooking for family, helping an old man).

1.2.1 Characteristics of Business Activities

Business activities possess distinct characteristics:

- An Economic Activity: Conducted with the aim of earning money or livelihood, not out of emotion.

- Production or Procurement of Goods and Services: Business enterprises either manufacture goods or acquire them from producers for sale to consumers. Goods can be consumables or capital goods; services include transportation, banking, etc.

- Sale or Exchange of Goods and Services: Involves the transfer or exchange of goods and services for value. Production for personal consumption is not business.

- Dealings in Goods and Services on a Regular Basis: Business requires repeated transactions; a single sale or purchase does not constitute business.

- Profit Earning: A primary objective, as no business can survive long without profit. Businesses strive to maximize profits by increasing sales or reducing costs.

- Uncertainty of Return: Refers to the unpredictability of the amount of profit that will be earned, with the possibility of losses.

- Element of Risk: The uncertainty associated with potential loss, caused by unfavorable events like changes in consumer taste, production methods, strikes, competition, natural calamities, etc. Risks cannot be entirely eliminated.

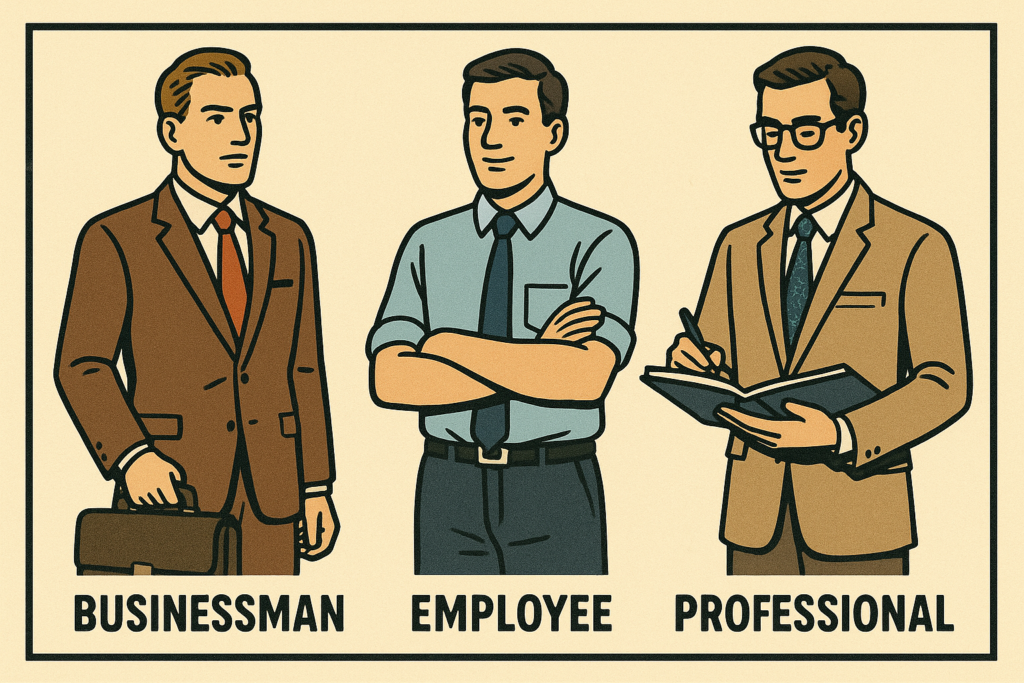

1.2.3 Comparison of Business, Profession, and Employment

Economic activities are categorized by key differences:

| Basic | Business | Profession | Employment |

| Mode of Establishment | Entrepreneur’s decision, legal formalities | Membership in professional body, certificate of practice | Appointment letter, service agreement |

| Nature of Work | Provision of goods and services | Rendering personalized, expert services | Performing work as per service contract/rules |

| Qualification | No minimum qualification necessary | Qualifications, expertise, training prescribed by professional body | Qualification and training as prescribed by employer |

| Reward/Return | Profit earned | Professional fee | Salary or wages |

| Capital Inv. | Required as per size and nature of business | Limited capital needed for establishment | No capital required |

| Risk | Profits uncertain, irregular; risk present | Fee generally regular, certain; some risk | Fixed, regular pay; no or little risk |

| Transfer | Possible with formalities | Not possible | Not possible |

| Code of Conduct | No prescribed code of conduct | Professional code of conduct to be followed | Norms of behavior laid down by employer to be followed |

| Example | Shop, factory | Legal, medical profession, chartered accountancy | Jobs in banks, insurance companies, government departments |

1.3 Classification of Business Activities

Business activities are broadly classified into Industry and Commerce.

1.3.1 Industry

- Industry refers to economic activities that convert resources into useful goods. It typically involves mechanical appliances, technical skills, and includes producing, processing goods, and breeding/raising animals.

- It also refers to groups of firms producing similar goods (e.g., cotton textile industry). Services like banking and insurance are also sometimes referred to as industries.

- Industries are divided into three categories:

- Primary Industries: Concerned with extraction and production of natural resources, and reproduction/development of living organisms.

- Extractive Industries: Extract products from natural sources, supplying basic raw materials (e.g., farming, mining, lumbering, hunting, fishing).

- Genetic Industries: Engaged in breeding plants and animals for further reproduction (e.g., seeds/nursery companies, cattle breeding farms, poultry farms, fish hatcheries).

- Secondary Industries: Use materials extracted by primary industries to produce goods for final consumption or further processing.

- Manufacturing Industries: Produce goods by processing raw materials, creating form utilities. They convert raw or partly finished materials into diverse finished products. Sub-categories based on operation method include:

- Analytical Industry: Analyzes and separates different elements from the same material (e.g., oil refinery).

- Synthetical Industry: Combines various ingredients into a new product (e.g., cement).

- Processing Industry: Involves successive stages for manufacturing finished products (e.g., sugar, paper).

- Assembling Industry: Assembles different component parts to make a new product (e.g., television, car, computer).

- Construction Industries: Involved in building construction, dams, bridges, roads, tunnels, and canals, requiring engineering and architectural skills.

- Manufacturing Industries: Produce goods by processing raw materials, creating form utilities. They convert raw or partly finished materials into diverse finished products. Sub-categories based on operation method include:

- Tertiary Industries: Provide support services to primary and secondary industries and trade, often considered part of commerce as auxiliaries to trade. Examples include transport, banking, insurance, warehousing, communication, packaging, and advertising.

- Primary Industries: Concerned with extraction and production of natural resources, and reproduction/development of living organisms.

1.3.2 Commerce

- Commerce includes two activity types: trade and auxiliaries to trade.

- Trade is the buying and selling of goods.

- Auxiliaries to Trade (Services): Activities that facilitate the purchase and sale of goods, such as transport, banking, insurance, communication, advertisement, packaging, and warehousing.

- Commerce connects producers and consumers by removing hindrances (persons, place, time, risk, finance, information) in the exchange process.

- Trade removes the hindrance of persons (making goods available to consumers).

- Transport removes the hindrance of place (moving goods).

- Warehousing removes the hindrance of time (storage).

- Insurance provides protection against risks of loss or damage.

- Banking and finance provide necessary capital.

- Advertising and public relations provide information and persuade customers.

1.4 Objectives of Business

- An objective is the starting point of business, representing what business people aim to achieve.

- While profit is often considered the primary objective, it is not the sole one. Profit is essential for:

- Source of income for business persons.

- Source of finance for expansion.

- Indicator of efficient working.

- Society’s approval of business utility.

- Building business reputation.

- However, businesses, as part of society, must fulfill multiple objectives for long-term survival and prosperity, including social responsibility.

- Key objectives beyond profit include:

- Market Standing: Maintaining goodwill and reputation, offering competitive products at reasonable prices, and ensuring customer satisfaction.

- Innovation: Introducing new ideas or methods in how things are done or made, or modifying existing products to enhance operation. This includes innovation in products/services and in skills/activities.

- Productivity: Ascertained by comparing the value of output to input.

1.5 Business Risk

- Concept of Business Risk: Business risk is the possibility of losses or insufficient profits due to unpredictable factors in business operations. It’s the chance of negative events impacting a business’s objectives or finances. Though inherent and unavoidable, risk can be managed.

- Causes of Business Risks: Business risks stem from a variety of sources:

- Natural Causes: Risks arising from unforeseen natural calamities or environmental changes beyond human control.

- Examples: Earthquakes, floods, droughts, famines, cyclones, etc.

- Human Causes: Risks originating from human behavior, actions, or inactions within or outside the business.

- Examples: Employee dishonesty (theft, embezzlement), strikes or lockouts, negligence, mismanagement.

- Economic Causes: Risks associated with changes in the economic environment and market conditions.

- Examples: Fluctuations in demand, price changes, increased competition, technological changes, inflation or deflation, economic recession.

- Political Causes: Risks arising from changes in political stability, government policies, or legislative frameworks.

- Examples: Changes in government regulations, political instability, war, civil unrest.

- Other Causes (Miscellaneous/Unforeseen):

- Examples: Mechanical failures, industrial accidents, unforeseen operational contingencies, sudden exchange rate fluctuations.

- Natural Causes: Risks arising from unforeseen natural calamities or environmental changes beyond human control.

1.6 Starting a Business — Basic Factors

Starting a business requires careful consideration of various factors to ensure its success and sustainability:

- Selection of Line of Business:

- Deciding the specific goods or services to offer, based on market demand, personal interest, skills, and resources.

- Size of the Business (Scale of Operation):

- Determining the scale of operation (small, medium, or large), influenced by market demand, capital availability, technology, and risk tolerance.

- Choice of Form of Ownership:

- Selecting the legal structure (e.g., sole proprietorship, partnership, company) based on liability, capital needs, continuity, and ease of formation.

- Location of Business Enterprise:

- Choosing the geographical placement, which impacts access to raw materials, labor, markets, infrastructure, and supporting services.

- Financial Requirements:

- Estimating capital needs (fixed and working capital) and identifying sources of finance (owner’s funds, loans).

- Physical Facilities:

- Ensuring the availability and efficient arrangement of physical resources like machinery, equipment, buildings, and utilities (power, water).

- Competent and Committed Workforce:

- Planning for, recruiting, training, and retaining a skilled, competent, and motivated employee base.

- Tax Planning:

- Strategically planning to optimize tax burden and ensure compliance with applicable tax laws.

- Launch of the Enterprise:

- The final step of commencing operations, requiring coordinated execution of all prior planning, including resource procurement, staffing, production setup, and initial marketing.